Semiconductors, once a behind-the-scenes technology, have now become one of the most talked-about building blocks of the modern economy.

But what exactly is a semiconductor? And why is demand for it growing so fast?

The answer lies in how deeply chips are woven into our everyday lives. As industries race to become faster, smarter, and more connected, their reliance on advanced chips continues to surge.

From powering AI models and data centers to enabling 5G networks, electric vehicles, and smart devices, semiconductors sit at the heart of nearly every digital experience.

That demand is showing up clearly in the numbers.

According to Statista, the global semiconductor market revenue is projected to reach $891 billion by 2026, driven by explosive demand for AI infrastructure, cloud computing, automotive electronics, and next-generation consumer devices.

So if you’ve ever wondered what semiconductors really are, and which top semiconductor companies are leading this high-stakes, high-growth industry in 2026, you’re in the right place.

In this blog we’ll discover:

- What Is a Semiconductor?

- List of the Top Semiconductor Companies In 2026

- Innovation Trends Shaping the Top Semiconductor Companies

- Challenges Faced by the Top Semiconductor Companies

What Is a Semiconductor?

In simple terms, semiconductors are the brains behind electronic devices. They allow phones, laptops, cars, and AI systems to process information, store data, and perform tasks.

Semiconductors work by acting as tiny electrical switches. These switches turn on and off billions of times per second, allowing devices to:

- Process information

- Make decisions

- Store data

This on–and–off behavior is what enables everything from sending a text message to running powerful AI models. The more switches a chip has, and the faster they operate, the more powerful the device becomes.

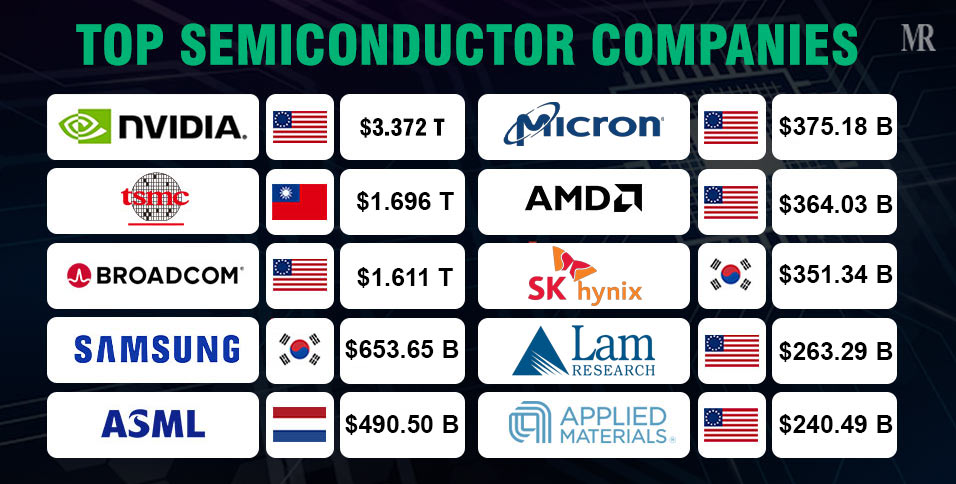

Now let’s look at the 10 top semiconductor companies ranked by their market cap.

List of the Top 10 Semiconductor Companies In 2026

Note: The market cap data is referred from the companiesmarketcap.com website as of January 2026.

| Company Name | Country | MarketCap | Core Products |

| 1. NVIDIA | USA | $4.458 T | AI Accelerators & Superchips: Massive GPUs (Blackwell/Rubin), ARM-based CPUs (Vera), and DPU/NIC networking silicon (BlueField/ConnectX). |

| 2. TSMC | Taiwan | $1.696 T | Logic Wafers (Foundry Services): 2nm (N2) nanosheet transistors and 3nm (N3P/X) FinFET wafers, plus CoWoS 3D-packaging services. |

| 3. Broadcom | USA | $1.611 T | Merchant & Custom Silicon: High-bandwidth Ethernet switch chips (Tomahawk 6) and custom AI ASICs co-designed for hyperscale cloud providers. |

| 4. Samsung | South Korea | $653.65 B | Memory & Logic Foundry: HBM4 (High Bandwidth Memory), 1c-node DRAM, and 2nm GAA (Gate-All-Around) manufacturing for mobile/AI chips. |

| 5. ASML | Netherlands | $490.50 B | Lithography Systems: High-NA EUV (EXE series) and Standard EUV (NXE series) machines that use light to “print” atomic-scale chip circuits. |

| 6. Micron Technology | USA | $375.18 B | Compute Memory & Storage: HBM3E stacks for GPUs, high-speed DDR5 server RAM, and ultra-dense 232-layer vertical NAND flash storage. |

| 7. AMD | USA | $364.03 B | High-Performance Processors: Data center CPUs (EPYC Turin/Venice), AI accelerators (Instinct MI350X), and consumer Ryzen AI processors. |

| 8. SK Hynix | South Korea | $351.34 B | Advanced AI Memory: 16-layer HBM4 modules for next-gen supercomputing and 321-layer QLC NAND for AI-optimized solid-state drives (eSSDs). |

| 9. Lam Research | USA | $263.29 B | Fabrication Equipment: Specialized “Etch” and “Deposition” machines used to drill deep vertical channels in 3D memory and logic chips. |

| 10. Applied Materials | USA | $240.49 B | Materials Engineering Tools: Systems for “Pattern Shaping” (Sculpta), transistor metallization, and backside power delivery for advanced nodes.manufacturing equipment and materials for chip production |

1. NVIDIA Corporation

- Market Cap (2026): $4.458 Trillion

- CEO: Jensen Huang

- Founded: 1993

- Core Products: Data-center GPUs (H100, H200, B200 variants), China-compliant AI accelerators, automotive AI platforms

NVIDIA is the biggest semiconductor company in the world and their AI chips power the world’s most advanced computing systems.

Founded in 1993, it entered the market through gaming graphics but became globally famous in the 2010s when its GPUs proved far superior for artificial intelligence and large-scale data processing.

By 2026, NVIDIA is the undisputed backbone of AI infrastructure. Its best-selling product, the Blackwell B200 GPU, is a specialized AI accelerator designed to process trillions of parameters; it functions as a “super-processor” that can train massive Large Language Models (LLMs) and run real-time AI reasoning at 25 times the energy efficiency of previous generations.

NVIDIA’s dominance is driven by its presence in the data centers of every major tech giant, including Microsoft, Amazon, Google, and OpenAI. Its hardware doesn’t just calculate; it connects. Using proprietary NVLink technology, NVIDIA allows thousands of these chips to communicate as a single, massive “super-chip,” providing the scale necessary for the next generation of autonomous vehicles, drug discovery, and climate modeling.

The company’s primary competitive advantage is its “moat”, a combination of unmatched hardware performance and CUDA, a mature software ecosystem that has become the industry standard for AI developers. Today, NVIDIA is not just a hardware vendor; it is a geopolitical heavyweight, central to global debates over technological sovereignty and the future of artificial intelligence.

2. TSMC

- Market Cap (2026): $1.696 Trillion

- CEO: C.C. Wei

- Founded: 1987

- Core Products: Advanced chip manufacturing (3nm, 5nm), logic chips for smartphones, AI, and high-performance computing

TSMC (Taiwan Semiconductor Manufacturing Company) is the world’s largest semiconductor companies and most advanced chip manufacturer and the second top semiconductor company. Unlike competitors who design their own silicon, TSMC is a “pure-play” foundry, meaning its sole mission is the flawless execution of other companies’ designs.

By 2026, TSMC’s 2nm (N2) node has entered volume production, utilizing Gate-All-Around (GAA) transistors for the first time. This technology is the industry’s “gold standard,” providing a 30% reduction in power consumption for the flagship chips in the iPhone 17 and NVIDIA’s next-generation architectures.

TSMC’s competitive advantage is its “yield leadership”, the ability to produce millions of perfect chips with minimal waste. Its CoWoS packaging has become a bottleneck for the AI industry; because TSMC is the only company capable of “stacking” logic and memory at this scale, the entire AI boom literally waits in line for TSMC’s factory slots.

3. Broadcom Inc.

- Market Cap (2026): $1.611 Trillion

- CEO: Hock Tan

- Founded: 1961 (current Broadcom formed in 2016)

- Core Products: Networking chips, data-center connectivity, broadband and enterprise semiconductors

Broadcom is the king of “data in motion.” While NVIDIA builds the “brains” that think, Broadcom builds the “nervous system” that allows data to travel between those brains at light speed.

Broadcom’s flagship product is the Tomahawk 6 Ethernet Switch. This chip handles a staggering 102.4 Terabits per second, allowing data centers to flatten their network architecture from three layers to two. This reduces the latency (delay) that often causes AI models to stutter during training.

Broadcom is the world leader in Custom ASICs (Application-Specific Integrated Circuits). Instead of buying off-the-shelf chips, giants like Google (TPU) and Meta (MTIA) hire Broadcom to co-design custom silicon.

By owning the networking standards (Ethernet) and the custom design pipeline, Broadcom makes itself a “systemic pillar” that cloud providers cannot bypass. This makes broadcom 3rd among the top semiconductor companies.

4. Samsung

- Market Cap (2026): $653.65 Billion

- CEO: Kyung Kye-hyun (Semiconductor Division)

- Founded: 1969

- Core Products: Memory chips (DRAM, NAND), smartphone processors, consumer electronics semiconductors

Samsung is the world’s largest memory chip producer and a major force in consumer electronics. It entered the semiconductor market decades ago and became globally dominant in memory chips during the 2000s, supplying storage and memory for devices worldwide.

While its foundry faces stiff competition from TSMC, Samsung remains the dominant force in the Memory Supercycle.

The hero product for Samsung in 2026 is HBM4 (High Bandwidth Memory). AI chips are useless without memory that can feed them data fast enough; HBM4 solves this “memory wall” by stacking 16 layers of DRAM directly on top of the processor.

Samsung’s HBM4 is unique because it uses 4nm logic dies, making the memory itself “smart” enough to handle basic processing before data even reaches the GPU.

Samsung’s advantage is vertical integration. By 2026, it has successfully ramped its 2nm GAA process in its Taylor, Texas fab

For customers looking to reduce their reliance on Taiwan (geopolitical hedge), Samsung offers a “one-stop shop” where they can get the most advanced memory and the most advanced manufacturing in a single contract.

5. ASML

- Market Cap (2026): $490.50 Billion

- CEO: Christophe Fouquet

- Founded: 1984

- Core Products: Lithography machines used to manufacture advanced chips

ASML is the only company in the world capable of producing the most advanced chipmaking machines. It entered the market in the 1980s but rose to global prominence in the 2010s when chipmakers began relying on its extreme ultraviolet (EUV) lithography machines to produce smaller, faster, and more energy-efficient chips.

Without ASML’s technology, modern processors used in AI, smartphones, and high-performance computing would not be possible. This makes it one of the top semiconductor companies.

ASML’s latest flagship product is the High-NA(High Numerical Aperture) EUV machine. Costing roughly $380 million per unit, this machine uses a completely redesigned optical system to shrink chip features by another 1.7x compared to standard EUV.

This precision is what allows companies like Intel and TSMC to move into the “Angstrom Era,” packing over 200 billion transistors onto a single processor.

ASML’s competitive advantage is a 100% market monopoly on the high-end equipment used by foundries. Its “moat” is built on 30 years of R&D and a supply chain of over 5,000 specialized partners that no other company can replicate.

6. Micron Technology

- Market Cap (2026): $375.18 Billion

- CEO: Sanjay Mehrotra

- Founded: 1978

- Core Products: DRAM and NAND memory chips

Micron is the premier U.S. manufacturer of memory and storage, playing a critical role in the “Reshoring” of the American semiconductor supply chain. The company gained prominence as demand for memory expanded with the rise of personal computers, smartphones, and later cloud computing, positioning Micron as a key supplier across multiple technology cycles.

Micron’s standout product is its HBM3E (High Bandwidth Memory). While Samsung and SK Hynix fight for volume, Micron has carved out a niche with energy efficiency.

Its 12-high 36GB HBM3E stacks provide 50% more capacity than previous generations while consuming 30% less power than competitors. This makes Micron the preferred choice for liquid-cooled AI data centers where thermal management is the primary operational cost.

Micron’s advantage is its 1-beta (1β) manufacturing process, which allows it to produce high-density memory without needing the most expensive EUV machines for every layer.

This keeps their costs lower and yields higher, making them a high-margin, strategically vital partner for NVIDIA’s H200 and Blackwell lines.

7. AMD

- Market Cap (2026): $364.03 Billion

- CEO: Lisa Su

- Founded: 1969

- Core Products: CPUs, GPUs, AI accelerators for PCs, servers, and data centers

AMD is known for designing high-performance processors that compete directly with industry leaders in PCs and servers. Under Lisa Su, AMD has transitioned from a “value alternative” to a performance leader in high-performance computing (HPC).

The 2026 flagship is the Instinct MI350X Accelerator. Built on the CDNA 4 architecture, this chip is designed to compete directly with NVIDIA’s Blackwell. It features a massive 288GB of HBM3E memory, which allows it to run massive models (like Llama 3) on fewer GPUs than competitors.

AMD’s open software approach with ROCm has finally matured, allowing developers to switch from NVIDIA with minimal friction.

AMD’s advantage is its Chiplet Leadership. By perfecting the art of “gluing” multiple smaller chips together, AMD can build massive, high-performance processors more cheaply and reliably than those trying to build one giant, single chip. This modularity allows them to pivot faster than anyone else in the industry.

8. SK Hynix

- Market Cap (2026): $351.34 Billion

- CEO: Kwak Noh-jung

- Founded: 1983

- Core Products: DRAM and NAND memory, high-bandwidth memory (HBM)

SK Hynix is the world leader in High Bandwidth Memory (HBM) and is 8th among the top semiconductor companies. While Samsung is a broader conglomerate, SK Hynix has a laser focus on the AI memory market, securing its position as the primary supplier for NVIDIA’s highest-end systems.

SK Hynix has successfully commercialized HBM4, the first memory to use TSMC’s logic base dies, by 2026. This collaboration has created a “super-memory” that can transfer data at over 1.5 Terabytes per second. It is currently the only company achieving high yields on 16-layer stacks, which are essential for the next generation of “Rubin” GPUs.

Its competitive advantage is Advanced Mass Reflow Moulded Underfill (MR-MUF) technology. This specialized packaging process allows SK Hynix to dissipate heat much better than its rivals, allowing their memory to run at higher speeds for longer periods without failing. Which is a requirement for the 24/7 training cycles of global AI giants.

9. Lam Research

- Market Cap (2026): $263.29 Billion

- CEO: Tim Archer

- Founded: 1980

- Core Products: Semiconductor manufacturing equipment

Lam Research is famous for making equipment used to manufacture and process chips. While it doesn’t produce chips itself, it has become increasingly important as chipmaking has grown more complex.

They are the world leaders in Etch and Deposition. If you imagine a chip is like a high-rise building, Lam provides the tools that drill the elevator shafts and the equipment that coats the walls with conductive metal.

Lam’s most critical innovation is Lam Cryo™ 3.0. As memory makers strive to reach 1,000 layers of 3D NAND (the storage in your phone and AI servers), they must drill perfectly straight holes through hundreds of layers of silicon.

Traditional drills generate too much heat, causing the holes to slant. Lam’s cryogenic technology freezes the wafer to ultra-low temperatures, allowing for high-aspect-ratio etching with atomic precision.

Lam’s competitive advantage is its dominance in the memory market. Nearly every 3D NAND flash chip in the world is processed using Lam equipment. Its “Equipment Intelligence” software uses AI to predict when a machine might fail, ensuring that multibillion-dollar factories never stop running.

10. Applied Materials

Applied Materials is one of the world’s largest suppliers of chipmaking equipment. They specializes in Materials Engineering, which is the science of manipulating atoms to create new types of transistors.

The company’s hero product in 2026 is the Centura® Sculpta®. This machine solves a massive problem: EUV lithography (from ASML) is getting so expensive that chipmakers want to use it less.

Sculpta is a “pattern-shaping” tool that can take a single pattern and stretch it to create the same density that previously required two expensive EUV steps. This saves manufacturers like Intel and Samsung up to millions per factory in capital costs.

Applied Materials has the broadest portfolio in the industry, making them rank 10 on the list of the top semiconductor companies in the world. They are essential for the transition to Gate-All-Around (GAA) transistors at the 2nm node.

Their Xtera™ Epi system is the only tool capable of depositing the source and drain materials in the tiny trenches of a GAA transistor without creating air bubbles (voids), making them the primary gatekeeper for next-generation mobile and AI processors.

Innovation Trends Seen in the Top Semiconductor Companies

The semiconductor industry is transitioning from general-purpose scaling to application-specific optimization. As Moore’s Law hits physical and economic limits, innovation is shifting toward architectural modularity and specialized silicon.

- Sub-3nm Lithography and Gate-All-Around (GAA) Transistors:

Moving to 3nm and 2nm nodes isn’t just about size; it’s a fundamental shift in transistor structure. By adopting GAA architectures, chipmakers are reducing “current leakage,” allowing for significantly higher clock speeds and lower thermal output in hyperscale data centers and premium mobile devices.

- Heterogeneous Integration and Chiplet Ecosystems:

The industry is moving away from monolithic “System-on-Chip” (SoC) designs toward chiplets. By interconnecting smaller, specialized dies using advanced packaging (like 3D-IC), manufacturers can mix-and-match nodes like placing critical logic on expensive 3nm nodes while keeping memory on mature, cost-effective nodes to maximize yield and reduce time-to-market.

- Domain-Specific AI Accelerators (NPUs):

General-purpose CPUs and GPUs are being augmented by Neural Processing Units (NPUs). These are hard-wired for the matrix multiplication required by Large Language Models (LLMs), delivering orders-of-magnitude improvements in “performance-per-watt” compared to traditional architectures.

- Wide Bandgap (WBG) Semiconductors for Power Electronics:

In the automotive and energy sectors, Silicon is being replaced by Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials handle higher voltages and temperatures with minimal energy loss, which is essential for extending EV range and improving the efficiency of solar inverters.

Challenges Faced by the Top Semiconductor Companies

Despite strong demand, the top semiconductor companies faces several growing challenges, such as:

- The “Billion-Dollar Barrier” in Fabrication:

The capital expenditure required for a leading-edge “Mega-Fab” has surpassed $20 billion. This extreme cost creates a high barrier to entry, consolidating the leading-edge market into a handful of players and increasing the financial risk of even minor cyclical downturns.

- The Specialized Skill Gap:

There is a critical shortage of VLSI (Very Large Scale Integration) engineers and materials scientists. As chip design becomes more complex (moving into 3D structures), the lack of human capital is becoming a more significant bottleneck than the availability of raw materials.

- Geopolitical Decoupling and Resource Nationalism:

The shift toward “onshoring” and “friend-shoring” is fragmenting the global supply chain. Tariff on chips and trade restrictions on EUV (Extreme Ultraviolet) lithography tools and critical minerals (like neon or gallium) are forcing companies to redesign supply routes, often at the cost of operational efficiency.

- The ESG Mandate for “Green” Fabrication:

A single modern fab can consume millions of gallons of water daily and gigawatts of power. With intensifying regulatory scrutiny, the industry is under pressure to implement circular water systems and carbon-neutral manufacturing processes without sacrificing throughput.

Conclusion

The world’s top semiconductor companies sit at the center of modern technology, enabling everything from AI data centers and smartphones to electric vehicles and cloud infrastructure.

Industry leaders such as NVIDIA, TSMC, Samsung, ASML, and AMD are not just large by market value; they occupy critical positions across design, manufacturing, memory, and equipment. This makes them essential to the functioning of the global digital economy.

As demand for advanced chips continues to rise in 2026, these companies stand out because of their scale, technological depth, and strategic importance.

Some dominate performance and AI computing, others control manufacturing capacity or irreplaceable tools, while memory leaders support the data-intensive workloads driving growth.

Together, the top semiconductor companies define the pace of innovation, influence supply-chain stability, and shape the future of computing, reinforcing why leadership in this industry carries both economic and geopolitical significance.

Maria Isabel Rodrigues